hidden

-

Welcome To

Paragon Investing

An Introduction For Prospective Clients

Paragon Offers Private & Alternative Investments

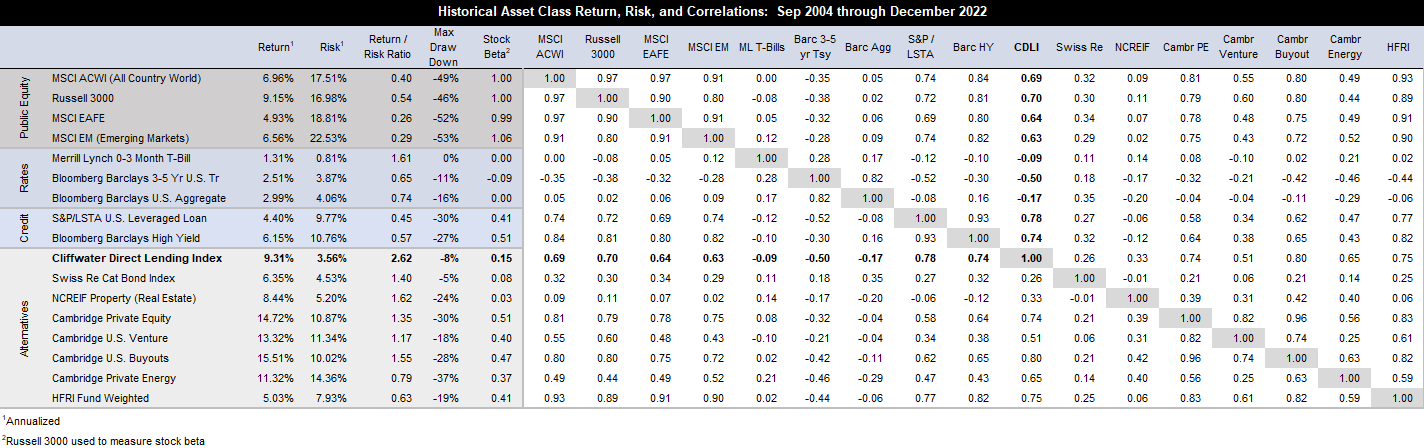

- From 2004-2022, the average Private Debt & Private Equity investment outperformed its public market equivalent by +5.9% per year, returning an average of 12.0% compared to an average of 6.1% for public Stocks & Bonds (Source).

- Public Stocks have returned 9.2% annually, while

- Private Equity has returned 14.7% annually, a +5.5% outperformance

- Source: Cambridge Private Equity Index vs Russell 3000, Oct 2004 - Dec 2022

- Public Bonds have returned 3.0% annually, while

- Private Debt has returned 9.3% annually, a +6.3% outperformance

- Source: Cliffwater Direct Lending Index vs Barclay's U.S. Aggregate Bond, Oct 2004 - Dec 2022

- Historically, the max quarterly loss (peak to trough) for Private Equity (-30%) is lower that of Public Stocks (-46% Russell 3000), and the max loss for Private Debt (-8%) is half that of U.S. Aggregate Bonds (-16%) for the period of Oct 2004 - Dec 2022 (Source).

The downside to private/alternative investments is threefold:

- Illiquidity: private investments are generally illiquid, meaning you cannot withdraw your capital for a period of time. At Paragon, this is usually a 3-month period.

- Limited access: historically, most private investments were only available via Limited Partnership (LP) deals with $1M stated minimums and extended lock-ups. Now, many funds will only work with clients through select investment advisors like Paragon.

- Small size: Funds that make private investments are much smaller in size, around $1.0B on average, and can only accept a limited amount of new money at a time.

- The upside of all these restrictions, is that it allows fund managers to identify and invest in what they view as the very best deals, allowing them to invest selectively to achieve higher returns (higher yields) and lower losses.

Inside A Paragon Investment Portfolio

Since the early 2000s, investors have benefited from access to private markets to increase returns and reduce risk. Paragon clients have access to restricted, semi-liquid, interval funds that invest in Private Debt and/or Private Equity.*

Within each portfolio, we employ a combination of semi-liquid private assets and liquid public investments, based on each client's liquidity needs and desire for increased return:

An illiquid 60/40 portfolio with 60% Private Equity and 40% Private Debt has historically provided a 12.5% return, nearly double the 6.7% return of traditional public 60/40 portfolio with 60% Stocks and 40% Bonds ( Source).

{kind=link}

* Some funds have high stated minimums (>$1M initial investment), but these minimums are reduced to $50k per fund and $100k overall when you invest with Paragon. Some funds are illiquid and some may be limited to accredited investors only.

** 60% allocation to 14.7% annualized + 40% allocation to 9.3% annualized = 12.5% return (private) vs 60% allocation to 9.2% annualized + 40% allocation to 3.0% annualized = 6.7% return (public); Equal risk: -21% max drawdown (private) vs -22% max drawdown (public), using a negative correlation for Bonds and +12% upside.

Levels of Service

At Paragon, we offer two different levels of service to cater to our clients' diverse needs. Pricing starts at an annual fee of 1.00% on your portfolio balance —- or $1,000 per year for every $100,000 invested with us. Higher balances receive lower fee rates, down to 0.45%.

Our two service tiers and fee rates are as follows:

- Access Only: For investors who want access to private investments for a portion of their portfolio, but don't need financial planning or regular meetings, this service costs 0.65% annually for a $1M portfolio, or 0.45% annually for a $5M portfolio.

- Full Service: For clients who want the complete suite of investment and financial services we offer and more face time with their advisor. Includes custom portfolio management, financial planning, comprehensive tax loss harvesting, and annual meetings. This service costs 0.80% annually for a $1M portfolio, or 0.60% annually for a $5M portfolio.